How do I stop VAT flat rate?

You can choose to leave the scheme at any time. You must leave if you’re no longer eligible to be in it. To leave, write to HMRC and they will confirm your leaving date. You must wait 12 months before you can rejoin the scheme.

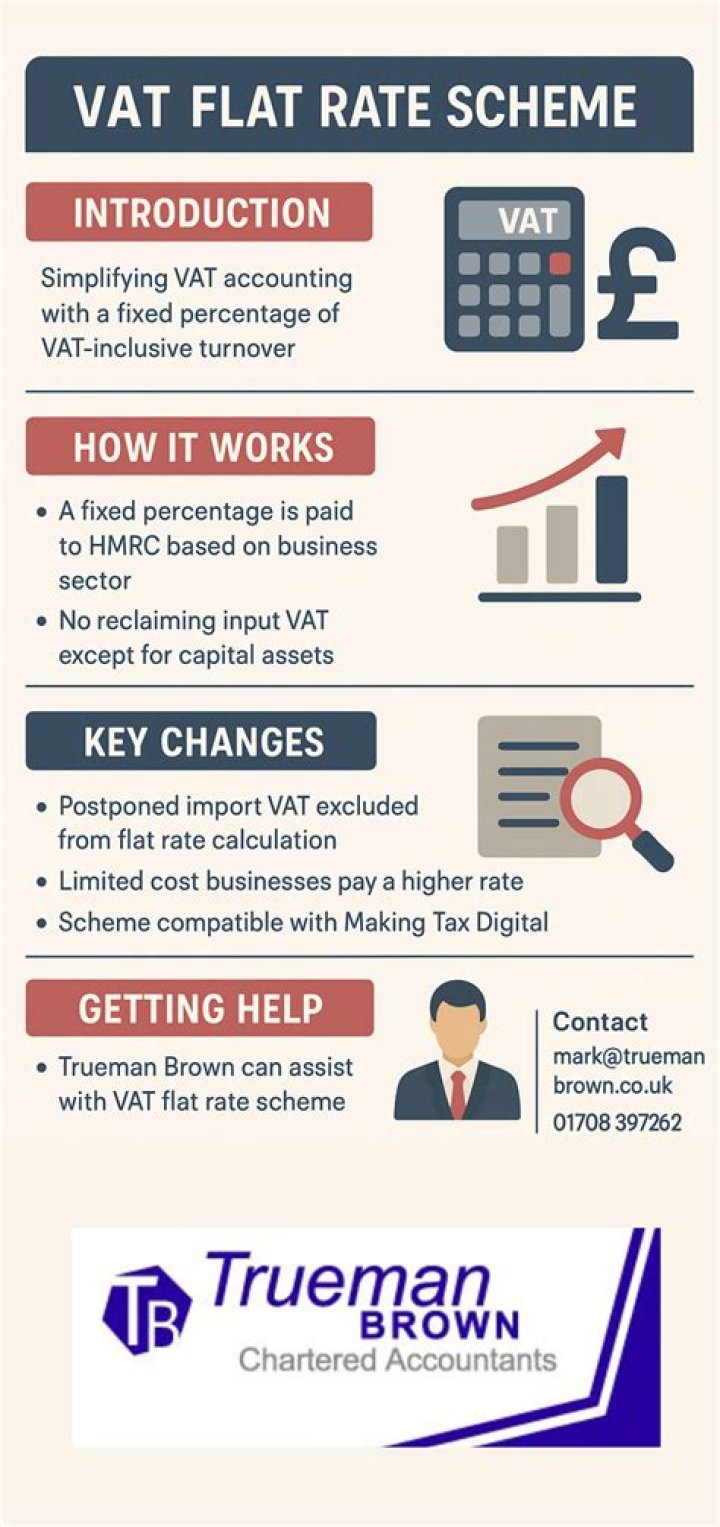

What is VAT flat rate scheme for small businesses?

The Flat Rate Scheme is an alternative way to pay your VAT to HMRC, which can save you valuable time when it comes to your quarterly bookkeeping. Instead of paying the difference between the VAT you charge customers and the VAT you reclaim on business purchases, you can pay a fixed rate based on your total sales.

Can I claim VAT back on the flat rate scheme?

You can’t reclaim VAT when you’re using the Flat Rate Scheme, unless you buy a capital asset that cost over £2,000 including VAT – you can reclaim the VAT on that, but must pay standard VAT on that asset when you sell it on. The VAT Flat Rate Scheme is designed to save a small business time, rather than cash.

Who is eligible for VAT flat rate scheme?

You can join the Flat Rate Scheme if: you’re a VAT -registered business. you expect your VAT taxable turnover to be £150,000 or less (excluding VAT ) in the next 12 months.

How long does it take to deregister from VAT?

Normally it usually takes three weeks for HMRC to confirm your de-registration and the official de-registration date (ie when the reason for your cancellation took effect, for example, you stopped trading, or when you asked to de-register if this was voluntary).

Can I change my VAT scheme?

You have no legal right to change to a different scheme – it’s up to HMRC to decide if they’ll grant your request. Once you’ve filled out the information online, or with form VAT484, HMRC will review your business situation and will make a decision on whether you can swap schemes.

What is the VAT threshold for 2021?

The VAT threshold currently stands at £85,000 for 2021/22 tax year in the United Kingdom. You must register with HMRC if your VATable turnover trips the threshold for Value Added Tax. Remember, these sales tax thresholds operate on a rolling 12-month period.

How far back can you claim VAT on assets?

On goods, you can reclaim VAT up to 4 years after you made the purchase. For services, you can reclaim VAT up to 6 months after the purchase.

What happens if I deregister for VAT?

From your de-registration, you must stop charging VAT, but retain your VAT records for six years, because HMRC may ask for them. HMRC will automatically re-register your business if it believes you shouldn’t have cancelled. And you’ll have to pay any VAT you should have paid.

Can I re register for VAT after deregistration?

You can claim for VAT after de-registration by completing form VAT 427 and sending it to HMRC. You should make your claim as soon as possible after de-registration. If your business bank account has been closed, then there could be a delay in any payments you are owed.

When can I change my VAT scheme?

When to change VAT schemes As per HMRC guidelines, you can only join a new VAT scheme at the start of a new accounting period. So we recommend changing your VAT scheme after you’ve produced your final VAT Return for the previous scheme.